Section oneEnergy

Introduction

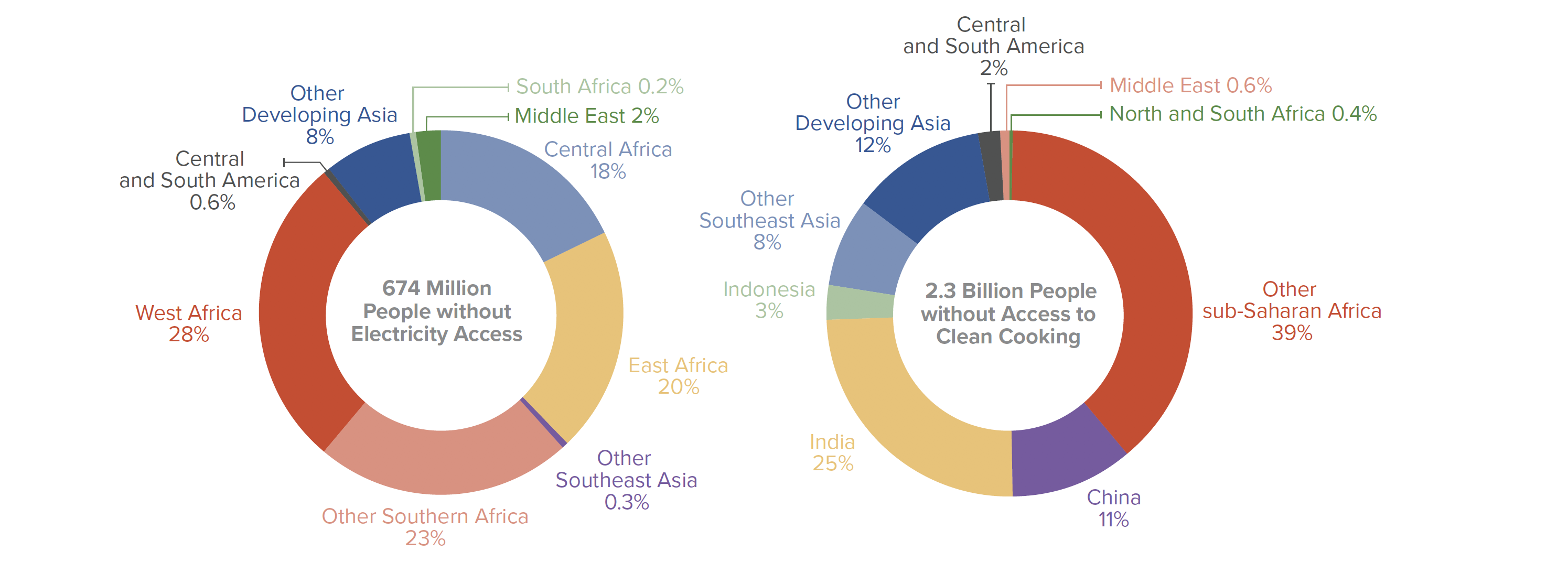

Energy is ingrained in all aspects of human life: It is how we power our homes, schools, and hospitals, our businesses, factories, and transport. But today, 1 billion people live without access to electricity, and nearly 3 billion people live without access to clean cooking.1 Even in developed economies, an estimated 200 million people, over 15% of the population, suffer from energy poverty.2 Fossil fuels, which have been instrumental in powering growth to date and currently account for 80% of global primary energy consumption,3 have resulted in economies that are vulnerable to volatile fuel prices and reliant on energy imports. Fossil fuels are also responsible for 75% of GHG emissions,4 as well as outdoor air pollution which is responsible for 4.2 million deaths per year.5

“Ensuring access to affordable, reliable, sustainable, and modern energy for all” (SDG 7) is fundamental to our economies and human development.6 The challenge is not only to meet our current energy needs, but also those of a projected 10 billion people by 2050 and to do so with low-cost, zero-carbon energy.7 By the end of the century, estimates point to a tripling or quadrupling of energy demand globally.8 Given the inextricable links of the energy-food-water nexus, growing energy demand and the energy challenge need to be considered in the broader context of wise water management (see Section 4) and sustainable food and land use (see Section 3). Together, they will significantly shape the global economy.

Transitioning to a low-carbon energy system to meet our current and growing needs is not only technically feasible but also economically and developmentally desirable.9 Reducing fossil fuel use, for instance, can improve human health and well-being and lower public health expenditures. According to analysis for this Report, over 700,000 premature deaths due to air pollution globally could be avoided compared with business-as-usual in 2030 under a global climate action scenario (see Box 4 on modelling).10 Additionally, switching to low-carbon energy sources – mostly by decarbonising power and electrifying a broader set of economic activities, first in buildings and light-duty urban transport (see Section 2.C), and then in heavy-duty transport and industry (see Section 5.C) – could deliver roughly two-thirds of the carbon emissions reduction required from the energy sector by 2040 to meet a 2˚C trajectory,; energy efficiency improvements could contribute the remaining third, according to the Energy Transitions Commission.11

Many technologies that can accelerate the energy transition over the coming decades are already known, proven, and starting to be deployed at scale; yet impediments remain. Effective policies are needed, both to incentivise private investment in low or zero-carbon innovation, such as carbon pricing (see Section 1.A), as well as to directly fund research, development, and demonstration of clean energy technologies, sometimes in partnership with the private sector (see Section 5.D). For example, evolving digitizing, smart-grid and battery technologies can play a significant role in enhancing the flexibility of the grid and its ability to swiftly tailor supply to meet demand or vice versa.12 Continued technological innovation and deployment will remain key. But enabling policies are evolving too slowly to incentivise the required system changes.13

Carbon pricing offers a significant economic prize. Under a scenario of global energy reform, modelled for this Report using the E3ME model (which introduces carbon pricing in line with the prices recommended in the 2017 High-Level Commission on Carbon Prices, a phase-out of fossil fuel subsidies, and financial support for the introduction of renewables), carbon pricing revenues and fossil fuel savings to reinvest in public priorities could be approximately US$2.8 trillion in 2030. In this global energy reform scenario, emissions would also be expected to fall by almost 24% relative to the baseline in 2030.14 Other benefits from this scenario would include an acceleration in the pace of economic activity, net employment generation, enhanced government budgets and improved health outcomes, among others. Despite the potential benefits of carbon pricing policies, at a global level, their use remains limited and has low impact today.

While we have a long way to go, momentum behind the shift away from fossil fuels is rapidly building with the pace of change varying from region to region, depending on legacy infrastructure and local resources. Overall, the cost of solar and wind is plummeting, down by 86% and 67% between 2009 and 2017, respectively.15 Even unsubsidised renewable energy is increasingly becoming cost-competitive with fossil fuel power generation in more and more places. As a result, the deployment of renewables is accelerating in many regions of the world: The world now adds more renewable power capacity annually than from all fossil fuels combined.16 Ensuring reliability of supply when the sun isn’t shining and the wind isn’t blowing remains a challenge, but storage technologies that facilitate the integration of intermittent renewables into the grid are increasingly available at low cost, as the price of batteries has halved over the past three years.17 Combined with other sources of flexibility, like existing dispatchable hydro and better demand response enabled by the ‘Internet of Things’ and the deployment of smart grid features, these technologies will make it possible to manage a near-total renewable power system by 2035 in most geographies.18 Nuclear and gas (provided methane leakage are under control) will provide a bridge to a zero-carbon future, especially in geographies with more limited renewable energy resources. Carbon capture utilisation and storage (CCUS) is unlikely to play a significant role in power decarbonisation, as it will struggle to compete with increasingly cost-competitive renewables, but it may be critical in some hard-to-abate industrial applications (see Box 50 on CCUS).19

In parallel, the rate of energy productivity improvement has started to accelerate, rising from 1.4% per annum over 1990-2005 to 1.7% over the past decade,20 mainly due to rapid progress in China (see Box 1 for China’s outsized role in the energy transition). Reducing energy waste across the buildings, industry, and transport sectors contributes to ramping up global economic productivity; as does increasing resource efficiency, especially efficient use of energy-intensive services, such as energy production (see Section 1.B), freight transport (see Section 5.C) and products, such as steel (see Section 5.A).

The energy transition needs to be carefully managed, both to ensure that existing contradictory or incoherent policies are reformed and to ensure a just transition for affected workers and communities. While the shift to a low-carbon and resilient economy will create jobs, it will also be essential to ensure that the transition is just for workers, particularly for incumbent industries and sectors where the shift to cleaner energy will cause, along with other systemic forces like automation, employment numbers to fall. In the United States, for example, 151,000 people are employed in fossil fuel power generation, with an additional 887,000 people in extraction (74,000 in coal, 310,000 in gas, and 503,000 in oil).21 Nearly half that number – about 476,00o people – are employed in solar and wind in the United States,22 even though these sectors currently constitute less than 10% of the power mix.23 It is expected that reduced employment in fossil fuels through the transition can be more than offset by a rise in employment in renewables and construction. Under the E3ME global climate action scenario examined for this Report, low-carbon employment is set to rise by 65 million people by 2030, more than offsetting employment reductions in some declining sectors to lead to a net employment gain of 37 million jobs globally by 2030.24 Engaging affected workers and communities in social dialogue with industry and the government will be essential to ensure a just transition for individual workers and for regions where fossil fuel jobs are concentrated (see, for instance, examples of successes in managing the transition in Box 5). The size of the challenge is likely to be particularly acute in coal-rich emerging economies like India, where Coal India, a state-owned enterprise (SOE) that produces 80% of Indian coal, employs more than 300,000 people.25

It will also be essential to raise, steer, and blend finance towards low-carbon energy infrastructure (see Box 7). Finance has started to shift, especially around the disclosure agenda. The TCFD, in particular, raised awareness among investors about the risks associated with investments in fossil fuels, especially the potential for stranded assets as a result of enhanced climate policies and as the costs of competing renewables continue to drop (see Box 6). For example, estimates suggest if investments in fossil fuels to 2035 continue along current trends, and countries enact policies to achieve a 2°C pathway and the low-cost producers sell out their assets accordingly, then approximately US$12 trillion of financial value could vanish from their balance sheets in the form of stranded assets.26