We need to increase both the quantity and the quality of infrastructure investment, but major barriers persist. These include unfavourable policies and investment regulations, a lack of transparent and bankable project pipelines, inadequate risk-adjusted returns, a lack of viable funding models and often high transaction costs. Unlocking finance for sustainable infrastructure will require coordinated reforms across policies, institutions and practices in financial markets.

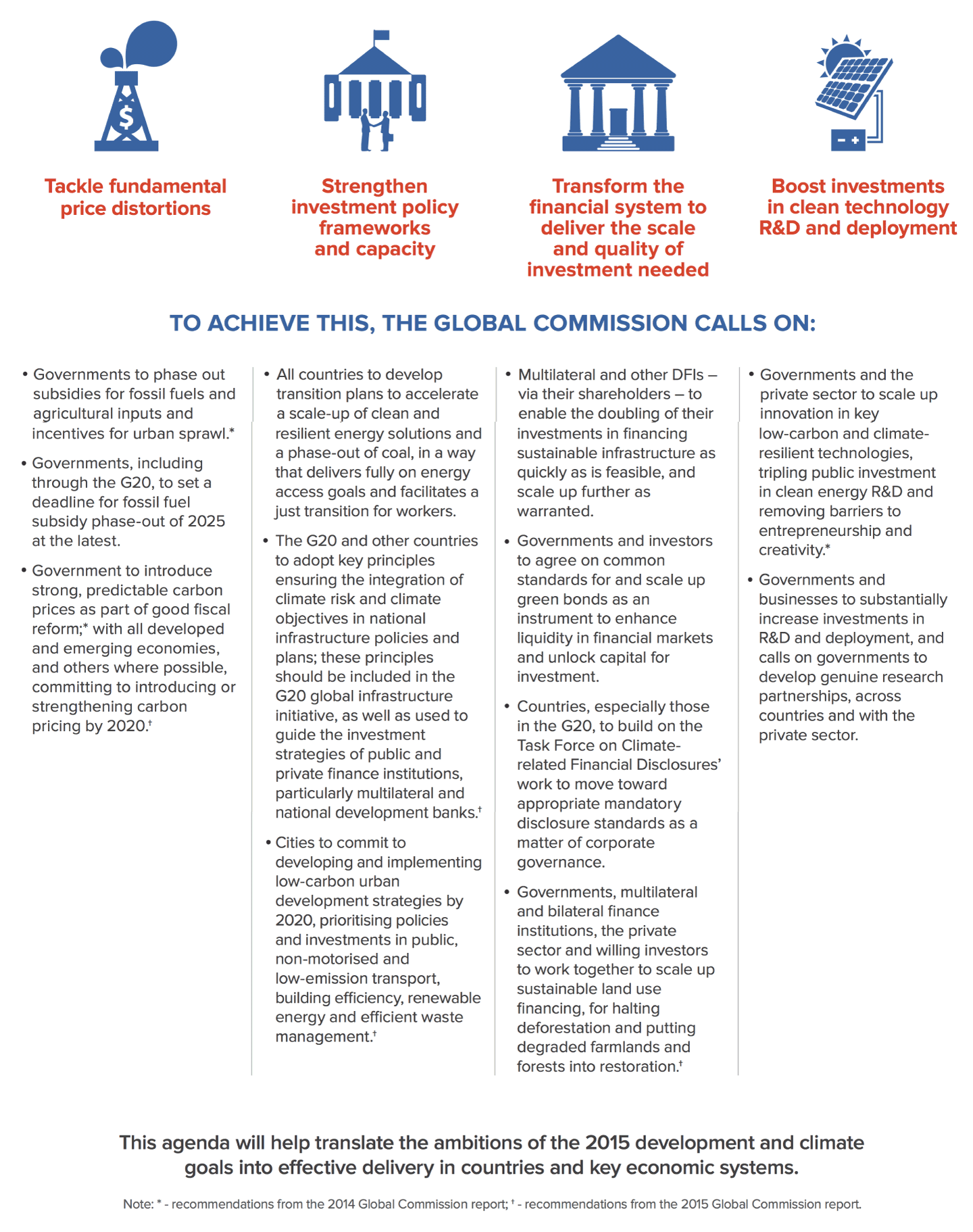

More money alone won’t do the job. Concerted action in four, inter linked areas can together help us overcome these barriers and build the sustainable infrastructure of the 21st century. Governments will play a leading role in shaping and directing action across these areas. The Global Commission emphasises the tticularly catalytic role that multilateral, regional and bilateral development finance institutions, as well as national development banks, can play in supporting countries and enabling a virtuous circle of action on sustainable infrastructure. In order to reach the scale of investments needed, however, the private sector will have an increasingly significant part to play in infrastructure investment.

First, we must collectively tackle fundamental price distortions – including subsidies and lack of appropriate pricing which leads to poor infrastructure investment decisions – to improve incentives for investment and innovation, and to generate revenue.

The Global Commission on the Economy and Climate has repeatedly emphasised the importance of phasing out fossil fuel subsidies (which amounted to around US$550 billion in 20142) and other distorting subsidies and tax breaks, such as those for water use, company cars and parking, and access to natural resources. Evidence is building of how successful reforms can free up scarce government revenues for other priorities, such as protecting poor households and managing the transition for affected sectors. For example, these savings can be channelled into programmes that benefit poor people, through better targeted income support and social safety nets, through investments in pro-poor infrastructure such as off-grid renewable energy solutions and energy efficiency, etc.

In the last three years, almost 30 countries have initiated or accelerated reforms of their fossil fuel subsidies, with many taking advantage of low oil prices to do so. Egypt, for instance, raised fuel prices by 78% in 2014 and plans to double them over the next five years; Canada has phased out several subsidies to oil, gas and mining, including ending targeted support to tar sands production; Indonesia raised gasoline and diesel prices by 33% in 2013 and another 34% in 2014; and India eliminated diesel subsides in October 2014 after incremental hikes. Given that subsidies to energy and fuel often particularly benefit middle- and high- income households, reforms can be progressive and channelling the savings into the right areas can benefit the poorest and most vulnerable in society.

While there is momentum, further reform is needed in both developed and developing economies. Both the G7 countries and North American leaders recently set a deadline of 2025 to phase out their fossil fuel subsidies. Other countries, including the G20, should follow suit. Many international institutions (such as the IMF, OECD, World Bank and IEA) have shown important leadership on this and are supporting progress in countries around the world.

The Global Commission also continues to emphasise the fundamental importance of strong, effective and rising carbon prices as a necessary condition for inclusive and low-carbon growth, in line with the Paris Agreement. Current pricing schemes collectively cover only about 12% of global GHG emissions, but a number of countries and companies have recently stepped up action, including through energy pricing reforms that effectively send a price signal to shift to cleaner energy solutions. Around 40 countries have implemented or scheduled carbon pricing. China, for example, will establish a national emissions trading system in 2017, expected to be the largest in the world. France adopted a carbon tax on transport, heating and other fossil fuels in 2014, and Vietnam took action in 2015 to adjust taxes, including on transport fuels, to better reflect their carbon content. Similarly, over 1,000 companies have now adopted an internal carbon price or plan to do so soon. Corporate leaders with pricing already in place include major consumer staples companies, such as Nestlé and Unilever; car brands, such as Mazda and General Motors; energy companies, such as Shell and BP; and financial giants, such as Barclays.

The Global Commission welcomes the emerging coalitions of governments, investors and businesses that have the potential to accelerate action globally on carbon pricing and fossil fuel subsidy reform, including by highlighting evidence of good practice and building multi-stakeholder partnerships for reform.

The Carbon Pricing Leadership Coalition, launched at COP21 in Paris, for example, is helping to build the evidence base on effective carbon pricing systems and share lessons learned. It brings together leaders from the public and private sectors, including from 26 governments, over 90 businesses, and more than 30 other strategic partners.

More broadly, pricing of infrastructure services should reflect the full costs of their provision, including where possible the social and environmental externalities. Lack of proper user charges for built infrastructure is a major impediment to attracting private investment, as private investors and operators require predictable and robust revenue streams to recover their costs. For public managed infrastructure, lack of appropriate pricing limits the availability of funds for properly maintaining the existing infrastructure or for extending service to those without access (e.g. to water, energy, roads and public transport). Overall, poor pricing leads to reduced service provision and quality. This can turn into a vicious circle, whereby infrastructure users are dissatisfied with the services, and thus reluctant to pay for them. For energy and urban systems, pricing is essential to reflect the social costs of externalities, for example the costs of air pollution from fossil fuel use as well as of congestion from urban vehicle use. For natural infrastructure and ecosystem services, pricing to reflect the value of these services can ensure efficient use, for instance, by reducing wasteful use of water or timber, and help secure finances to support local communities to invest in restoration and maintenance of the ecosystems.

Second, we must strengthen policy frameworks and institutional capacities to deliver the right policies and enabling conditions for investment, to build pipelines of viable and sustainable projects, to reduce high development and transaction costs, and to attract private investment.

Countries need a well-defined and appropriately designed pipeline of bankable, sustainable projects. But the capacity to develop and implement projects is low because of underlying issues such as poor planning, lack of mandate, skills shortages, inadequate regulatory frameworks for public-private partnerships and implementation, and weak enabling policy environments. Governments and development finance institutions are already working to expand capacity, but much more is required, including increased concessional finance for project preparation, and strengthened support for implementation within a broader policy reform process (such as measures to tackle inefficiencies, improve governance and combat corruption) which reaches beyond central government agencies to cover subnational and local-level entities.

Overall, governments have to make a greater effort to “invest in investment” – to improve public infrastructure planning, management, governance and policies. At the same time, to ensure sustainability over the long term, investment plans and project selection must better reflect environmental and social sustainability criteria. Governments should develop and implement procurement processes that incorporate sustainability criteria and are systematic and consistent in approach.

A stable and predictable policy and regulatory environment can attract investment in infrastructure, supported by stronger enabling environments for business, for example by enhancing competition, trade policies and corporate disclosure. Of particular importance is the need to strengthen governance frameworks, including anti-corruption measures. Public-Private Partnerships (PPPs) can help, if implemented well, to secure private engagement in sustainable infrastructure investment. Improving the institutional and regulatory frameworks for PPPs – including the transparency and credibility of processes for selection and agreement on projects, consistency of policy and implementation, and standardisation of contracts and documents – is essential to boost investor confidence and attract the scale of investment needed.

Clear national, subnational and sectoral development strategies, with accompanying infrastructure and investment plans, are essential to guide long term public and private investments. Leadership will be needed to monitor progress and ensure that these plans promote low-carbon and climate-resilient development, reflect the financial realities of each country, and are aligned with their Nationally Determined Contributions to achieve the 2°C goal in the Paris Agreement.

A number of countries are starting to take steps in the right direction. For example, Colombia is working to mainstream climate action across its national development plan and, amongst other pro-active measures, has established a focused programme on public-private collaboration, with priority attention to investment in infrastructure and achieving environmental sustainability. It has also put a range of fiscal incentives in place for investment in low- carbon technologies and environmentally resilient practices, such as in the forestry sector. In the area of resilience, Zambia has received US$1.5 million to support a sustainable investment strategy based on its development priorities through the Pilot Program for Climate Resilience, and is making good progress to broadly integrate resilience objectives into its national development planning.

In addition to national strategies, governments must also develop and implement sectoral plans that align with climate goals. Building support for these will not always be easy, especially given potential resistance from powerful incumbents who benefit from business-as-usual. The rapid transformation needed in the energy sector to meet climate goals is particularly challenging.

The Global Commission calls on all countries to develop transition plans to accelerate a scale-up of clean and resilient energy solutions and a phase-out of coal, in a way that delivers fully on energy access goals and facilitates a just transition for workers.

These transition plans should include both measures to ensure that clean energy solutions are economically attractive and affordable, and those that will better reflect the true costs of coal and other fossil fuels. The Global Commission welcomes the establishment of a Just Transition Centre that is initiated by the International Trade Union Confederation (ITUC) with emerging partnerships with business and civil society, focused on dialogue between governments, employers, workers and civil society around how to ensure a “just transition” towards including at national and sectoral levels.

Third, we must transform the financial system to deliver the scale and quality of investment needed in order to augment financing from all sources (especially private sources such as long-term debt finance and the large pools of institutional investor capital), reduce the cost of capital, enable catalytic finance from development finance institutions (DFIs), and accelerate the greening of the financial system.

The scale of financing requirements for sustainable infrastructure calls for a strengthening of resources from all sources: public and private, domestic and external. It will involve regulatory action, policies, better governance frameworks and business practices to harness capital markets and the financial system to deliver sustainable development.

Public finance, whether through domestic resources or through development finance, will remain fundamental to the provision of infrastructure, including by playing a catalytic role in attracting private finance. In developing and emerging economies, about 60–65% of the cost of infrastructure projects is financed by public resources, while in advanced economies this figure is around 40%.

National budget allocations to support sustainable infrastructure investment are essential and should increase. This will often include the use of revenues that countries raise themselves, for example through taxes, or other finance they are able to raise, including through bonds, loans, or through development finance institutions. Fossil fuel subsidy reform and carbon pricing, emphasised above, can also be important sources of capital for sustainable infrastructure. And whatever the source of financing, ensuring effective public spending, including through strong, transparent and green public procurement practices, can allow scarce public resources to achieve more.

Beyond public financing, there is real need to significantly scale up private financing to meet our infrastructure requirements. But there are real challenges in tapping adequate private investment and in bringing down the high costs of finance. Banks and local financial institutions are well suited to provide long term debt finance in the construction phase. There is also much greater scope to attract institutional investors through equity offerings and the development of local capital markets, including for “take-out” finance (where securitisation of initial debt occurs to make it long-term and attractive to institutional investors). Take-out finance can also help free up capital for more projects over time, since banks are able to sell a part of their loans to a third party and reinvest the money as projects become operational.

DFIs, including Multilateral and Bilateral Development Banks, can play a pivotal role in pioneering and scaling up financing models for sustainable infrastructure that can crowd in private finance. This is especially true in developing countries and in emerging economies, which often face prohibitively high costs of capital due to high perceived risks. For example, interest rates are as high as 18% in India for off-grid renewable energy financing through domestic capital markets. This must change, and can be facilitated through the use of innovative measures, such as more extensive use of guarantees, insurance and other de-risking instruments. In addition to the development and wider deployment of risk mitigation instruments, DFIs can play a role through the use of blended finance more generally (including concessional and non- concessional finance, and dedicated climate finance), and help create more viable and replicable financing models and tools (e.g. for credit enhancement and risk mitigation). Successful instruments and platforms should be replicated and scaled-up. There is also a need to emphasise the “development” role of DFIs, paying particular attention to the needs of less developed countries for whom the challenges of preparing, financing and executing sustainable infrastructure projects are particularly acute, rather than operating like commercial banks when assessing infrastructure investment risks.

Recognising their important catalytic role, the Global Commission calls on multilateral and other development finance institutions – via their shareholders – to enable the doubling of their investments in financing sustainable infrastructure as quickly as is feasible, and scale up further as warranted.

A number of DFIs are stepping up their investments already, including through measures to expand their capital base, blend finance from different sources and leverage private and other investment in sustainable infrastructure. They are also partnering with countries to strengthen policies, institutions and capacities to reliably deliver domestic resources and ensure a solid pipeline of bankable projects tailored to national priorities. The New Development Bank (BRICS Bank), for example, has recognised the imperative around sustainable infrastructure and is demonstrating initial leadership in this area. In April 2016, it launched its first four investments, worth US$811 million, all for clean energy projects. In July 2016, it announced its plans to issue green bonds worth approximately US$450 million. Other important steps are being taken by a number of DFIs, in particular to help crowd in other sources of finance. The European Bank for Reconstruction and Development (EBRD), for example, has played a significant role in accelerating energy efficiency. Since 2006, cumulative EBRD financing of Sustainability Energy Financing Facilities has reached more than €3.4 billion (US$3.7 billion) in over 100,000 sub-projects, involving more than 100 partner financial institutions in 24 countries, including large international banks and small banks in Central Asia and the Caucasus.

There is increasing potential to mobilise green finance to bolster support for low carbon and climate-resilient infrastructure through new tools and approaches like green bonds and green infrastructure. The green bond market reached U $42 billion in 2015. HSBC, working with the Climate Bonds Initiative, predicts that the amount could more than double this year. With the right approach, green bonds can be powerful instruments and play a tremendous role in facilitating sustainable infrastructure investment and growth. For example, the Philippines issued the first climate bond for a geothermal project in an emerging economy, as form of credit enhancement. The US$225 million-equivalent local currency bond comes in addition to a direct Asian Development Bank local currency loan of US$37.7 million equivalent. Such credit-enhanced project bonds offer an attractive alternative to bank financing, and can mobilise long-term capital to help close the region’s infrastructure gap. Applying global standards can ensure that the proceeds are used to finance projects with demonstrable climate or other environmental benefits.

The Global Commission calls on governments and investors to agree on common standards for and scale up green bonds as an instrument to enhance liquidity in nancial markets and unlock capital for investment.

A number of major investors, including pension funds and insurance companies, are already starting to shift their investments. For example, over 400 investors with US$25 trillion in assets have joined the Investor Platform for Climate Actions, committed to increasing low-carbon and climate-resilient investments, including by working with policy-makers to ensure financing at scale. The Norwegian Sovereign Wealth Fund, the largest in the world, has taken steps recently to divest from companies with large coal assets. Attracting more institutional investors to finance sustainable infrastructure would be a big prize, as they have in total an estimated US$100 trillion in assets under management.

While these examples are promising, further action is required to shift the financial system to support investment in sustainable infrastructure, including through the use of equity offerings, appropriate risk mitigation and development of local capital markets to provide the large sums that will be needed for take-out finance. Establishing some forms of infrastructure as a distinct asset class could also help make it a standard part of investment portfolios and unlock access to large pools of capital, such as from institutional investors.

Investors and shareholders can play a critical role in demanding that companies use environmental, social and governance (ESG) standards, and in considering these as the bottom line for investments. Simplification and standardisation of reporting requirements are both essential for transparency and to ensure that the climate risks that affect financial performance, including the physical risk of climate change and the potential for stranding high-carbon assets, are considered in investment decisions.

An industry-led task force, established under the Financial Stability Board at the request of G20 finance ministers, is drafting recommendations for voluntary measures to disclose climate-related financial risks. The Global Commission welcomes the work of the Task Force on Climate-related Financial Disclosures, and looks forward to its recommendations. Implementing such standards can help ensure that investors have all the information they need to assess whether a company’s capacity and strategies can generate value over time, including whether medium- and long-term business strategies align with the policy direction reflected in the Paris Agreement.

A number of countries are leading the way already. France, for example, has introduced mandatory corporate disclosure of climate information, which includes financial risks from climate impacts and carbon reporting across the supply chain. The Chinese central bank has proposed mandatory climate disclosure as part of a series of other reforms to help green its financial system.

The Global Commission calls on countries, especially those in the G20, to build on the work of the FSB Task Force on Climate-related Financial Disclosures to move toward appropriate mandatory disclosure standards as a matter of corporate governance.

The culture and incentives for financiers has started to change but should go further, for example to prioritise and value more sustainable long-term investments over a narrow focus on short-term gains. To enable this, we have to ensure that financial regulations such as capital and solvency rules do not inadvertently act as disincentives to participation by banks and institutional investors. Revamping the financial system will also require a “greening” of banks and their practices or, where existing institutions are insufficient, establishing green investment banks.