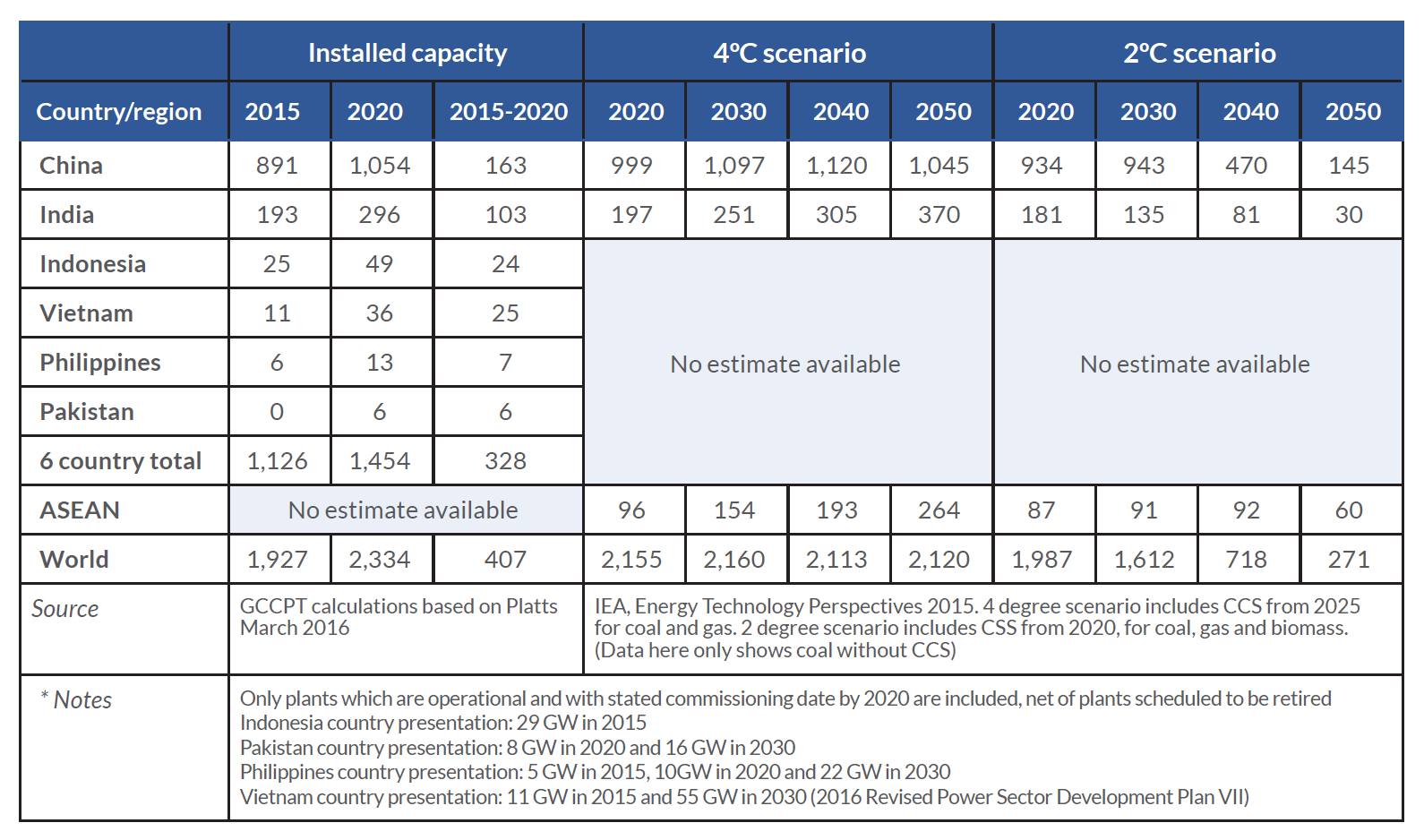

Box 18 — Understanding the full cost of fossil fuels

If countries are to invest in least-cost energy pathways, their planning processes need to account for the full range of costs and benefits of different options. Yet many energy system plans are based on outdated prices for renewable and energy efficiency technologies. They also reflect incomplete assessments of the local costs and benefits, as well as existing price distortions. As a result, many energy system investment plans still prioritise fossil fuels over clean energy.

A crucial cost that is often neglected is local air pollution. The risks to human welfare posed by local air pollution, in terms of economic and social costs, are increasingly well documented and far greater than previously understood.21 Outdoor air pollution, much of which is associated with fossil fuels, is linked to nearly 4 million premature deaths per year.22

China and India both face major challenges. In China, PM2.5 pollution from fossil fuel combustion and cement manufacture has been linked to a median estimate of 1.23 million premature deaths in 2010.23Updated estimates indicate air pollution killed around 1.6 million people in China in 2013, with an estimated 366,000 deaths from coal pollution alone. In India, the air pollution toll in 2013 stood at 1.4 million deaths.24 The problem is so severe that curbing local air pollution has become a policy priority. In Delhi, the local air pollution was so severe in 2015 that doctors were prescribing that patients with serious respiratory problems simply move out of the city.25

In Europe, research by the Health and Environment Alliance has shown that the impacts of coal plant emissions – mainly due to respiratory and cardiovascular conditions – account for more than 18,200 premature deaths, about 8,500 new cases of chronic bronchitis, and over 4 million lost working days each year. Adding emissions from coal power plants in Croatia, Serbia and Turkey, the figures for mortality increase to 23,300 premature deaths per year, or 250,600 life years lost.26

The economic costs associated with the health impacts of air pollution are also significant. Analysis for the Global Commission shows that the health and mortality burden of air pollution can be considerable, amounting to as much as 4% or more of GDP in some countries.27 Recent analysis by the OECD28 has found that globally, if we continue with business as usual, air pollution-related healthcare costs alone are projected to increase from US$21 billion in 2015 (using constant 2010 US$ and PPP exchange rates) to US$176 billion in 2060. By 2060, the annual number of lost working days, which affect labour productivity, are projected to reach 3.7 billion (from around 1.2 billion today) at the global level. The annual global welfare costs associated with premature deaths from outdoor air pollution are projected to rise from US$3 trillion in 2015 to US$18-25 trillion in 2060. In addition, the annual global welfare costs associated with pain and suffering from illness are projected to be around US$2.2 trillion by 2060, up from around US$300 billion in 2015.29 Thus, welfare costs of air pollution that are in the range of a few trillion dollars today are expected to be an order of magnitude higher by 2060, unless we make a major shift in the way we use energy and control air pollution. Considering the indirect costs of air pollution raises the costs even more: roughly doubling the costs of air pollution in the near-term and adding another order of magnitude of costs in the longer term due to a slowdown of economic growth.

Analysis by the IMF on the damages and costs caused by fossil fuels – through impacts such as air pollution, congestion, traffic accidents and climate change – shows that coal has the largest negative impact on human health through the pollution that it causes, and yet coal’s use is pervasively undercharged in terms of fuel taxes and carbon pricing.

Because fossil fuels are such a big part of the problem, replacing them with clean energy options can sharply reduce air pollution. A recent analysis found that doubling renewables in the global energy mix, instead of continuing with business as usual, could save up to 4 million lives annually by 2030.30 Moreover, the IMF estimates that removing subsidies and charging for externalities associated with fossil fuel use could cut global CO2 emissions by more than 20%, and cut premature deaths caused by air pollution by more than half.31

Integrating the full costs of air pollution on human health and productivity into energy and transport investment decisions would also help level the playing field between fossil fuels and clean energy options. For example, in large parts of Southeast Asia, coal-fired power costs as little as US$0.06-0.07 per kWh, but even conservative accounting for air pollution adds US$0.04 per kWh, bringing coal-fired power costs to US$0.10-0.11 per kWh and removing its price advantage over renewable power sources.32

Along with air pollution and CO2 emissions, the damages from the full life cycle of coal include land disturbance, fatalities in extraction and transport and methane and mercury emissions. Factoring all this into estimates of the cost of coal can double or triple its price; for example, in cost estimates based on coal from the Appalachia, in the US these costs add close to US$0.18 per kWh. This makes wind, solar and other forms of non-fossil fuel power generation, along with investments in energy efficiency, economically competitive.

While there are limitations to these estimates, it is clear that air pollution imposes a very serious cost on society, and it must be duly accounted for in economic assessments to avoid making irresponsible investment choices.33 The benefits of reducing air pollution can also be enjoyed in the near term, and accrue locally, mostly to the benefit of the country taking action. Governments should incorporate these cost estimates into the analyses that guide public investment decisions. Regulatory or price-based policies can ensure that the private sector does the same.